As solar power installations surge worldwide, a new industry is emerging from the shadows: solar waste recycling. With millions of photovoltaic (PV) panels expected to reach end-of-life in the coming decades, analysts warn that unmanaged solar waste could become a major environmental challenge.

At the same time, experts say solar waste recycling could unlock billions of dollars in recoverable materials, turning a looming disposal problem into a powerful economic opportunity.

Solar Waste Recycling

| Key Fact | Detail |

|---|---|

| Global solar waste by 2050 | Up to 60–78 million metric tonnes |

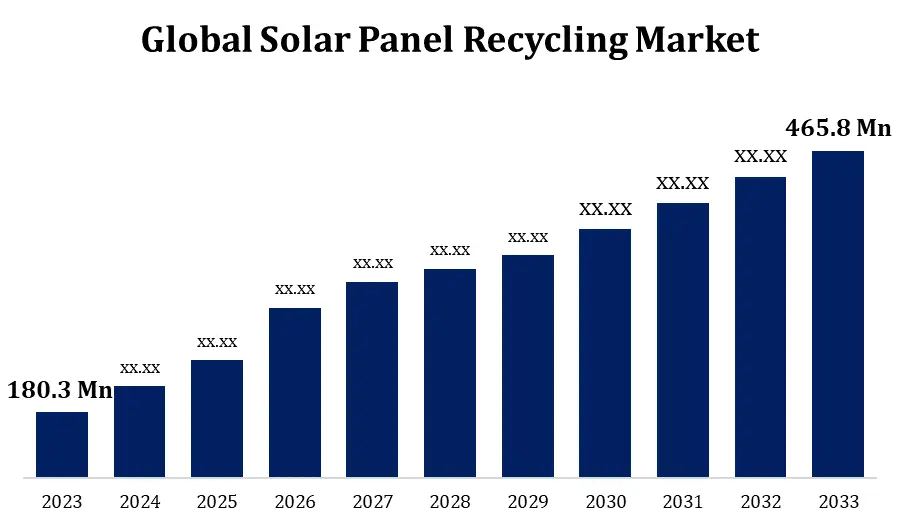

| Market value projection | Solar panel recycling could exceed $2–4 billion globally by 2030 |

| Material recovery rate | Up to 95% of panel materials can be recovered |

| India solar waste estimate | 11 million tonnes by 2047 |

Why Solar Waste Is the Next Big Industrial Challenge

Solar panels typically last 25 to 30 years. The first wave of large-scale installations from the early 2000s is now approaching retirement. According to the International Renewable Energy Agency (IRENA), global cumulative solar waste could reach between 60 and 78 million metric tonnes by 2050.

That waste contains valuable materials including:

- Silicon

- Silver

- Copper

- Aluminum

- Glass

- Rare metals such as indium and tellurium

If not recycled, panels can end up in landfills. While most PV panels are not classified as hazardous waste, improper disposal may lead to environmental contamination.

“Solar panels are not simply waste — they are material banks,” said an IRENA analyst in its end-of-life solar report. “Recycling can transform the economics of renewable energy.”

Understanding Solar Waste Recycling

Solar Waste Recycling refers to the industrial recovery of materials from decommissioned or damaged photovoltaic modules.

The recycling process generally involves:

1. Collection and Reverse Logistics

Panels are transported from utility farms, rooftops, and commercial installations to centralized facilities.

2. Mechanical Separation

Aluminum frames, junction boxes, and glass layers are separated using automated dismantling equipment.

3. Thermal and Chemical Treatment

Advanced processes extract high-value materials such as silicon wafers and silver contacts.

4. Refinement and Resale

Recovered materials are reintroduced into the solar manufacturing supply chain. According to industry estimates, up to 95% of panel materials are technically recoverable. However, economic feasibility depends on scale and technology.

The Market Forecast — From Niche to Multi-Billion Dollar Sector

Several research firms project strong growth in the solar recycling market:

- Fortune Business Insights estimates the market could exceed $3 billion by the early 2030s.

- Grand View Research projects a compound annual growth rate (CAGR) above 15%.

- Short-term forecasts suggest even faster growth as regulatory frameworks mature.

The expansion is being driven by:

- Rising solar installations

- Aging first-generation panels

- Raw material price volatility

- Environmental compliance mandates

- ESG investment flows

What was once a waste management issue is becoming an industrial opportunity.

India’s Solar Boom — And the Recycling Gap

India aims to reach 500 GW of non-fossil fuel capacity by 2030. Solar is central to this ambition. However, the Council on Energy, Environment and Water (CEEW) estimates India could generate 11 million tonnes of solar waste by 2047.

CEEW projects the recycling industry in India could be worth ₹3,700 crore (approximately $500 million) by 2047.

Currently, India has only a small number of commercial-scale solar recyclers. Infrastructure remains limited compared to projected waste volumes.

“India has an opportunity to build a domestic recycling ecosystem before the waste surge peaks,” said a CEEW researcher in its policy roadmap.

Why Investors Are Watching Closely

Solar waste recycling sits at the intersection of several high-growth themes:

1. Circular Economy (KW2)

Governments and corporations increasingly emphasize circular resource systems. Recycling aligns with global sustainability frameworks.

2. Critical Mineral Security (KW3)

Solar panels require silver, copper, and polysilicon — materials facing supply pressures. Recycling reduces dependence on mining.

3. ESG Investing (KW4)

Institutional investors are prioritizing environmental impact alongside returns. Recycling businesses score strongly on sustainability metrics.

According to the U.S. Environmental Protection Agency (EPA), structured solar recycling programs can create jobs while strengthening supply chains.

JSW Energy को मिला 230 MW रिन्यूएबल एनर्जी प्रोजेक्ट, Solar Energy Corp के साथ हुई बड़ी डील

Revenue Streams in Solar Waste Recycling

Entrepreneurs are exploring multiple business models:

Recycling Facilities

Large centralized plants capable of processing tens of thousands of tonnes annually.

On-Site Decommissioning Services

Field teams specializing in safe removal and transportation.

Material Brokerage

Selling recovered aluminum, copper, and silicon back to manufacturers.

Technology Licensing

Advanced chemical recovery processes that increase silver yield can command licensing fees.

Data and Asset Tracking Platforms

Digital systems that track panel lifecycle and compliance documentation. The industry is not limited to recycling plants alone. It spans logistics, engineering, metallurgy, software, and environmental services.

The Technology Race — Improving Recovery Economics

Early recycling methods focused mainly on recovering glass and aluminum. Newer technologies aim to recover:

- High-purity silicon

- Silver paste

- Rare metals

Companies in Europe and the United States are experimenting with:

- Robotic disassembly lines

- Chemical delamination techniques

- High-temperature processing systems

Improving material recovery rates directly improves profitability.

Industry analysts say the key challenge is lowering processing costs while increasing recovery efficiency.

Environmental and Climate Impact

Solar waste recycling reduces:

- Landfill use

- Resource extraction

- Energy consumption in mining

- Lifecycle carbon emissions

IRENA notes that recycled solar materials could significantly reduce future raw material demand, cutting environmental impacts associated with mining and refining. This aligns with global net-zero strategies and national sustainability goals.

Regulatory Landscape — A Critical Catalyst

Policy will likely determine the speed of industry growth.

Extended Producer Responsibility (EPR)

Some jurisdictions require manufacturers to manage end-of-life disposal.

European Union

The EU’s Waste Electrical and Electronic Equipment (WEEE) Directive includes solar panels.

United States

State-level initiatives are emerging, though no federal mandate yet exists.

India

India is still developing a comprehensive solar waste framework, though policy discussions are underway. Regulatory clarity reduces uncertainty and attracts capital.

हरियाणा के किसान मात्र ₹53,926 में लगवा सकते हैं 3 HP सोलर पंप, सब्सिडी से मिलेगा बड़ा फायदा

Risks and Challenges

Despite its promise, the industry faces hurdles:

- High initial capital expenditure

- Transportation costs

- Fluctuating metal prices

- Lack of standardized recycling protocols

- Limited consumer awareness

Experts caution that profitability depends on scale.

“Without sufficient volume, recycling facilities struggle to break even,” noted a clean-tech market analyst at a renewable energy conference.

Case Study — Early Movers in the Market

In the United States, companies such as Solarcycle have announced facilities capable of processing up to one million panels annually.

These operations integrate recycling with glass manufacturing, creating vertically integrated systems that reduce supply chain costs. Such models demonstrate how scale can improve margins.

Wealth Creation Potential — Hype or Reality?

The “multi-million dollar business idea” label is not marketing rhetoric alone. It reflects:

- Rapid solar adoption

- Predictable waste growth

- Recoverable high-value materials

- Growing policy support

- Global decarbonization commitments

However, wealth creation will likely concentrate among:

- Technology innovators

- Early infrastructure builders

- Firms securing long-term recycling contracts

- Companies achieving high recovery efficiencies

The sector may mirror early solar manufacturing — high growth, intense competition, eventual consolidation.

The Global Outlook to 2050

By mid-century, solar installations will multiply many times over. Waste generation will follow a predictable curve. Recycling capacity must scale accordingly.

Industry analysts suggest that by 2040:

- Solar recycling could become standard practice

- Recovered materials may supply a significant share of new panel inputs

- Countries lacking recycling capacity could face environmental and economic pressure

In that context, solar waste recycling is less an optional niche and more an inevitable industrial sector.

Related Links

Solar energy transformed the power sector. Now its by-products are reshaping the industrial landscape.

Solar Waste Recycling represents the convergence of sustainability, supply chain security, and entrepreneurship. As aging panels accumulate and material prices fluctuate, the ability to extract value from retired modules may define the next phase of clean energy economics.

Whether it becomes a multi-million or multi-billion dollar industry depends on technology, regulation, and scale.

But few analysts dispute that the sector’s growth is no longer a question of “if” — only “how fast.”