Australia’s Australia’s Green Hydrogen Vision strategy—exporting renewable energy in the form of green hydrogen, often called “liquid sunshine”—is advancing in 2026 as part of a broader push to become a global clean energy supplier.

Backed by major investments and international partnerships, the initiative aims to supply low-carbon fuel to Asia and Europe, although cost pressures, technological hurdles, and project delays continue to test its commercial viability.

Australia’s Green Hydrogen Vision

| Key Fact | Detail/Statistic |

|---|---|

| Hydrogen export target | 200,000 tonnes annually by 2030 |

| Long-term production goal | 15 million tonnes by 2050 |

| Major investment | Over AUD 20 billion committed to clean energy sectors |

Understanding Australia’s Australia’s Green Hydrogen Vision Strategy

Australia’s Green Hydrogen Vision initiative is built on its abundant renewable resources, particularly solar and wind energy. By converting this energy into hydrogen through electrolysis, the country aims to create a transportable, zero-carbon fuel for global markets.

Green hydrogen is produced by splitting water into hydrogen and oxygen using renewable electricity. Unlike fossil fuel-based hydrogen, it emits no carbon dioxide during production.

Energy analysts note that this model allows Australia to export renewable energy indirectly, overcoming the limitations of electricity transmission over long distances.

Why “Liquid Sunshine”?

The phrase “liquid sunshine” reflects the conversion of solar energy into hydrogen or hydrogen-derived fuels such as ammonia. Instead of exporting raw electricity, Australia can:

- Convert solar energy into hydrogen

- Liquefy or chemically transform it

- Ship it globally

This approach mirrors Australia’s success in exporting liquefied natural gas, but with significantly lower emissions.

Major Projects Driving the 2026 Push

Hydrogen Production Hubs

Australia has identified several hydrogen hubs to scale production:

- Western Australia: Focus on export-oriented projects

- Northern Territory: Strategic location for Asian markets

- Queensland: Integration with industrial demand

These hubs aim to build supply chains, infrastructure, and workforce capacity.

Large-Scale Export Projects

Among the most ambitious developments:

- Projects targeting millions of tonnes of hydrogen annually

- Integrated solar and wind farms dedicated to hydrogen production

- Export terminals designed for ammonia and liquid hydrogen shipping

Global Demand: Asia and Europe Lead

Australia’s hydrogen export strategy is driven by demand from energy-importing countries.

Asia-Pacific Markets

Japan and South Korea are leading hydrogen adopters, investing heavily in hydrogen-powered industries and energy systems. These countries lack sufficient renewable resources and are expected to rely on imports.

European Interest

European nations, particularly Germany, are also seeking green hydrogen imports to meet climate targets. Australia’s political stability and existing trade relationships make it a preferred partner.

Government Policy and Investment

National Hydrogen Strategy

The Australian Government has outlined ambitious targets:

- 200,000 tonnes of exports by 2030

- 15 million tonnes of production by 2050

These goals are supported by regulatory frameworks and funding initiatives.

“Future Made in Australia” Policy

The government has committed substantial funding to clean energy industries, including hydrogen. This includes:

- Production tax incentives

- Infrastructure investment

- Certification systems for green hydrogen

Economic Potential: A New Export Industry

Hydrogen is widely viewed as a potential replacement for fossil fuel exports.

Opportunities

- Job creation in regional areas

- Diversification of export revenue

- Strengthening of energy security

Industry projections suggest that hydrogen could become a multi-billion-dollar export sector.

सरकार की नई स्कीम,स्वदेशी सोलर पैनल पर मिलेगी ₹17,000 की और सब्सिडी, बस ध्यान रखें ये बातें

Technological Advancements Driving the Hydrogen Economy

As hydrogen production technologies improve, Australia’s competitive advantage in green hydrogen is growing. Key advancements in hydrogen electrolysis, storage, and transportation are pushing down costs:

- Electrolysis improvements: Increased efficiency in splitting water into hydrogen using renewable electricity. (scientificamerican.com)

- Storage technologies: Development of high-density storage systems for hydrogen at lower costs.

- Ammonia synthesis: Enhanced ammonia production processes that lower the energy required to create ammonia for shipping.

Challenges and Risks

High Production Costs

Green hydrogen remains expensive compared to fossil fuels. Key cost drivers include:

- Renewable electricity prices

- Electrolyser costs

- Infrastructure investment

Analysts indicate that cost reductions are essential for competitiveness.

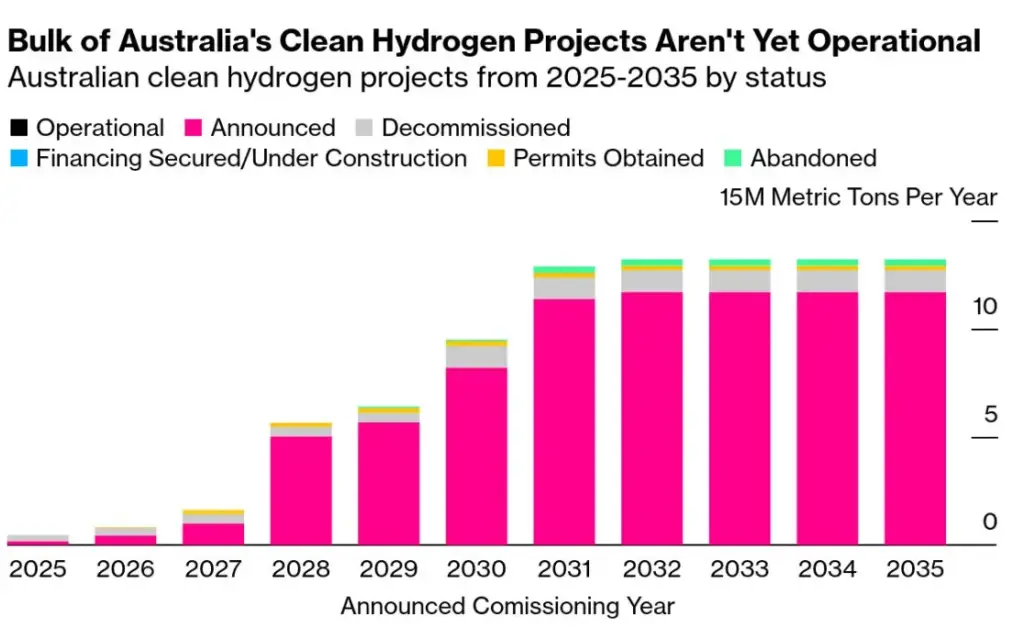

Project Delays and Uncertainty

Several high-profile projects have faced delays or cancellations due to:

- Rising capital costs

- Investor caution

- Uncertain long-term demand

These developments highlight the gap between policy ambition and market readiness.

Infrastructure Constraints

Hydrogen transport presents technical challenges. Options include:

- Liquefied hydrogen

- Ammonia conversion

- Chemical carriers

Each method involves trade-offs in efficiency and cost.

Environmental and Resource Considerations

While green hydrogen is considered clean, it is not without environmental concerns.

Water Usage

Hydrogen production requires significant water resources, raising concerns in arid regions of Australia.

Land Use

Large-scale renewable projects require vast land areas, potentially affecting ecosystems and local communities.

Lifecycle Emissions

Experts stress the importance of ensuring that hydrogen production remains fully renewable to achieve climate benefits.

International Collaborations and Partnerships

Australia’s green hydrogen vision is not limited to domestic policy. International partnerships are crucial for its success.

- Japan has signed agreements with Australia to import hydrogen as part of its decarbonisation efforts.

- Germany is looking to secure long-term hydrogen imports to meet its stringent climate targets.

- South Korea is another key player, working with Australian companies to integrate hydrogen into its industrial sectors.

These collaborations underscore Australia’s role as a future hydrogen supplier on the global stage.

Financial Backing and Private Investment

While government policy plays a crucial role, private sector investment will be pivotal in driving Australia’s hydrogen success.

- Major corporations, including Fortescue Metals and Woodside Energy, are heavily invested in Australia’s green hydrogen projects.

- Banks and institutional investors are also stepping in, providing capital to accelerate large-scale production.

These investments reflect confidence in hydrogen as a future energy source, but also highlight the high risks and costs associated with its development.

Community Engagement and Stakeholder Involvement

For green hydrogen projects to succeed, they need the support of local communities.

Engagement Efforts

- Consultation with Indigenous communities about land use for renewable energy production.

- Local job creation through workforce development programs for the renewable energy sector.

- Public awareness campaigns to highlight the long-term environmental and economic benefits of green hydrogen.

These initiatives help ensure that the growth of the hydrogen industry benefits both local and global stakeholders.

Expert Perspectives

Energy experts remain cautiously optimistic. Australia is “well positioned to scale green hydrogen production” due to its renewable resources and geography, according to recent industry analysis. However, analysts stress that success depends on:

- Reducing costs

- Securing long-term buyers

- Building infrastructure

Consumer and environmental groups, meanwhile, call for careful planning to ensure sustainability.

Related Links

NSW Battery Incentive 2026: How to Claim Your $2,400 Rebate Today

How Your Home Can Earn Money as a Power Station: The Rise of VPPs in Australia

What 2026 Means for the Industry

The year 2026 represents a transition phase for Australia’s hydrogen industry. Key developments to watch:

- Commissioning of pilot and mid-scale projects

- Expansion of export agreements

- Technological improvements in hydrogen production

Large-scale commercial exports are likely to take longer, with most analysts pointing to the late 2020s or early 2030s for significant volumes.

Australia’s Australia’s Green Hydrogen Vision ambition reflects a bold shift in global energy systems. While the country has strong advantages in renewable resources and policy support, the path to becoming a leading hydrogen exporter will depend on overcoming economic and technical challenges in the years ahead.