Alberta’s “$0 down solar” initiative, formally known as the Clean Energy Improvement Program (CEIP), is transforming how homeowners finance renewable energy upgrades.

By tying repayment to property taxes instead of traditional loans, the program removes upfront costs and expands access to solar energy, offering a government-backed model that is gaining attention across North America.

Alberta’s $0 Down Solar

| Key Fact | Detail |

|---|---|

| Financing Structure | Repayment via property taxes |

| Upfront Cost | No initial payment required |

| Repayment Period | Typically 10–25 years |

| Ownership Transfer | Loan stays with property |

As governments look for scalable ways to fund clean energy transitions, Alberta’s CEIP offers a model that blends public financing with private benefit. Its long-term success may depend on expansion, oversight, and continued public engagement.

Understanding the Alberta’s $0 Down Solar: Alberta’s $0 Down Solar Model

The Alberta’s $0 Down Solar, commonly referred to as Alberta’s $0 down solar model, reflects a broader shift in how clean energy is financed at the household level. The Clean Energy Improvement Program (CEIP) allows homeowners to install solar systems without paying upfront, replacing traditional loans with a property tax-based repayment mechanism.

The model is designed to address one of the most persistent barriers to renewable energy adoption: high initial costs. By spreading payments over decades and integrating them into property taxes, CEIP aims to make solar accessible to a wider segment of the population.

Energy policy experts say such models are essential to achieving long-term climate goals. “Upfront cost is the single biggest barrier to residential solar,” said a policy analyst at a Canadian clean energy think tank. “Programs like CEIP directly target that issue.”

How the CEIP Financing Model Works

Municipal Funding and Contractor Payments

Under CEIP, municipalities act as financial intermediaries. Once a homeowner is approved, the municipality funds the project and pays the contractor directly.

This structure ensures that:

- Contractors receive payment promptly

- Homeowners avoid complex financing arrangements

- Municipalities maintain oversight of project standards

Officials say this approach also improves consumer protection by requiring certified contractors and approved technologies.

Property Tax-Based Repayment System

The cost of the solar installation is added to the homeowner’s property tax bill as a special charge. Repayment is spread over a fixed term, typically between 10 and 25 years.

Because property taxes are a stable and enforceable revenue stream, municipalities can offer lower interest rates compared to unsecured loans. A municipal official involved in CEIP implementation noted, “The tax-based model reduces risk, which allows us to pass savings on to homeowners through better financing terms.”

Financing Linked to the Property

Unlike conventional loans, CEIP financing is tied to the property rather than the individual. If the home is sold, the remaining balance transfers to the new owner.

This feature is widely seen as a key advantage. It ensures that those who benefit from the solar system also share in its cost.

Financial Breakdown: What Homeowners Actually Pay

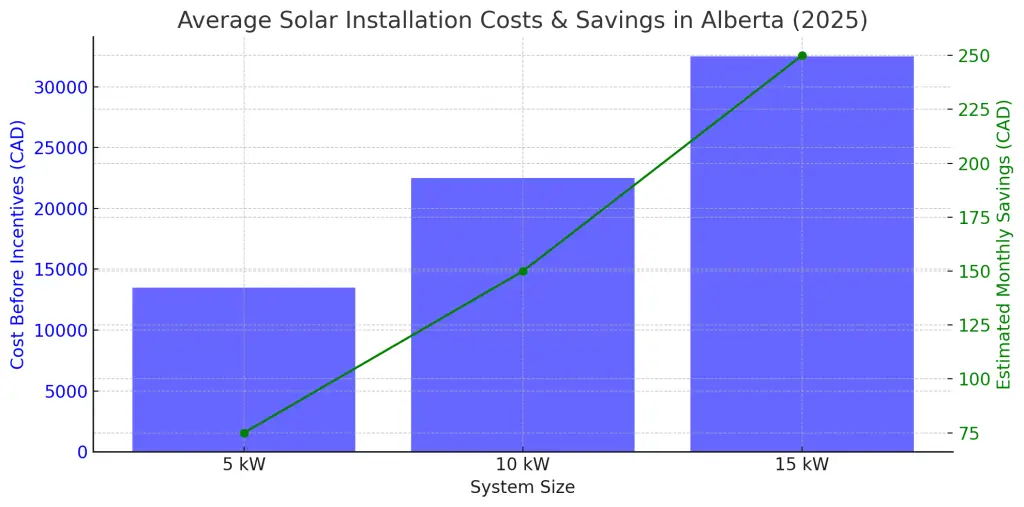

A typical residential solar installation in Alberta may cost between $15,000 and $25,000. Under CEIP:

- The full cost is financed

- Interest is applied at a fixed rate

- Payments are added annually to property taxes

For example:

- A $20,000 system over 20 years

- Annual repayment: approximately $1,200–$1,500

Electricity savings can offset a significant portion of these costs, depending on system size and energy usage.

Energy economists caution, however, that savings vary. “Solar economics depend on local electricity prices, system performance, and consumption patterns,” said an academic researcher in renewable energy finance.

Real-World Example: A Homeowner Perspective

In municipalities where CEIP is active, homeowners have reported increased willingness to invest in solar.

One Calgary resident, cited in municipal case studies, said the program made solar “financially possible” for their household. “We didn’t have $20,000 upfront, but the monthly impact through taxes felt manageable,” the homeowner noted.

Such examples highlight the program’s role in expanding access beyond higher-income households.

Comparison with Traditional Solar Financing

| Feature | CEIP Model | Traditional Loan |

|---|---|---|

| Upfront Cost | None | Often required |

| Interest Rate | Lower (municipal-backed) | Market-based |

| Approval Criteria | Property-based | Credit-based |

| Transferability | Stays with property | Stays with borrower |

This comparison underscores why CEIP is often described as more accessible than conventional financing options.

Broader Context: The Rise of PACE Financing

CEIP is part of a broader framework known as Property Assessed Clean Energy (PACE), which has been implemented in various U.S. states and Canadian regions.

PACE programs have financed billions of dollars in energy upgrades. According to industry reports, their success is tied to three factors:

- Long repayment periods

- Secure tax-based collection

- Alignment of cost with property value

However, some jurisdictions have faced criticism over consumer protections and disclosure practices, highlighting the importance of regulatory oversight.

Environmental and Policy Impact

Programs like CEIP contribute to reducing greenhouse gas emissions by accelerating the adoption of renewable energy.

Government data suggests residential solar installations can significantly lower household carbon footprints. When scaled across thousands of homes, the impact becomes substantial. Policy analysts say CEIP also supports local economic development by:

- Creating jobs in installation and maintenance

- Encouraging investment in clean technology

- Reducing strain on centralized power systems

Risks and Criticisms

Despite its benefits, CEIP is not without challenges.

Financial Risks

- Interest costs mean homeowners pay more over time

- Property tax increases may affect affordability

Market Risks

- Solar performance depends on weather and system quality

- Energy savings are not guaranteed

Policy Concerns

- Limited availability across municipalities

- Administrative complexity

Consumer advocates stress the importance of transparency. “Homeowners must fully understand the long-term financial commitment,” said a representative from a consumer protection organization.

Related Links

Victoria’s $1,400 Solar Upgrade: How the New ’10-Year Rule’ Benefits Homeowners

Ontario Solar Hack: How to Stack Enbridge HER+ Rebates with Federal Loans

Future Outlook

Municipal governments continue to evaluate CEIP’s effectiveness, with early indicators showing strong participation and low default rates.

Experts believe the model could expand to include:

- Energy-efficient retrofits

- Heat pumps

- Electric vehicle infrastructure

There is also growing interest in adapting similar programs globally, particularly in regions seeking to accelerate renewable energy adoption without heavy public subsidies.

FAQs

What is Alberta’s $0 down solar program?

It is the Clean Energy Improvement Program (CEIP), which allows homeowners to finance solar installations through property taxes without upfront payment.

Is CEIP available everywhere?

No, it is only available in municipalities that have adopted the program.

Are there interest charges?

Yes, the financing includes interest, though rates are typically lower than private loans.

What happens when a home is sold?

The remaining balance transfers to the new owner along with the solar system.