India’s solar industry is entering a decisive transition as new rules under the Approved List of Models and Manufacturers (ALMM) expand to include solar cells.

At the core of the “Made in India or Bust” debate is a structural shift: from June 2026, developers must rely on domestically manufactured cells, a move expected to reshape supply chains, project economics, and investment flows across the renewable energy sector.

Made in India or Bust

| Key Fact | Detail | Impact |

|---|---|---|

| Policy Trigger | ALMM to include solar cells from 2026 | Mandatory domestic sourcing |

| Cost Impact | Tariffs may rise ₹0.40–₹0.50/unit | Higher power prices |

| Supply Risk | Domestic capacity initially insufficient | Project delays possible |

| Strategic Goal | Reduce import dependence | Boost manufacturing |

India’s expansion of ALMM to include solar cells represents a defining shift in its renewable energy strategy. The policy moves the sector from cost-led growth to strategic self-reliance, with implications for tariffs, supply chains, and investment flows.

While the transition may bring short-term disruption, its long-term success will depend on how quickly domestic manufacturing scales and how effectively stakeholders adapt. The outcome will shape not only India’s solar future but also its position in the global clean energy economy.

Understanding the Made in India or Bust Policy Shift

The Approved List of Models and Manufacturers (ALMM), overseen by the Ministry of New and Renewable Energy (MNRE), ensures only approved manufacturers supply equipment for solar projects. With the inclusion of solar cells:

- Developers must procure domestically manufactured cells.

- Imported cells are effectively restricted.

- The entire upstream supply chain comes under policy control.

This marks a shift from a cost-optimised global sourcing model to a policy-driven domestic ecosystem.

Demand vs Supply: The Core Structural Challenge

Projected Demand Surge

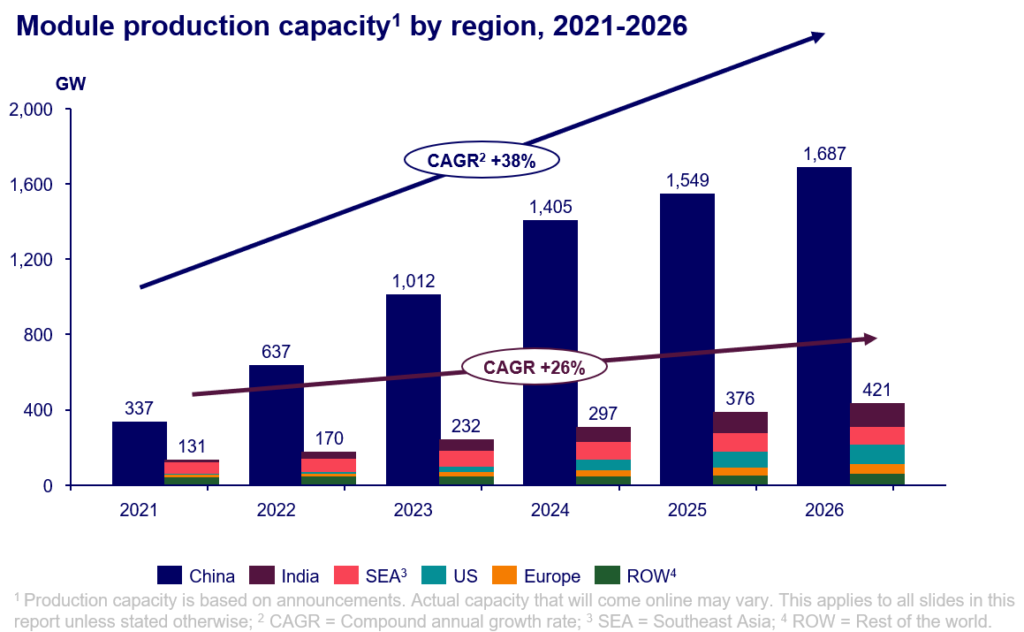

India is expected to add 30–40 GW of solar capacity annually over the next few years to meet its 2030 targets.

Domestic Capacity Reality

Current solar cell manufacturing capacity:

- Significantly below projected demand.

- Concentrated among a few large players.

- Still scaling under government incentives.

This mismatch is the central risk in the transition.

Technology Gap: The Hidden Constraint

Shift Toward Advanced Cells

Global markets are rapidly moving toward:

- TOPCon (Tunnel Oxide Passivated Contact).

- HJT (Heterojunction Technology).

However, India’s domestic manufacturing is still catching up in these technologies.

Why This Matters

If domestic manufacturers lag in advanced cell efficiency:

- Developers may face performance trade-offs.

- Levelised cost of energy (LCOE) may increase.

- Competitiveness of Indian solar projects may decline.

Cost Implications: Beyond the 50 Paisa Narrative

Capex Pressure

Developers face:

- Higher module costs due to expensive cells.

- Increased logistics and procurement costs.

- Potential penalties from project delays.

Tariff Impact

Industry estimates indicate:

- ₹5–10 million/MW increase in capex.

- ₹0.40–₹0.50/unit increase in tariffs.

But analysts stress that this is a range, not a certainty.

Financing Impact: Banks and Lenders Turn Cautious

Rising Cost of Capital

Banks and financial institutions are likely to:

- Increase risk premiums.

- Demand higher equity contributions.

- Tighten lending conditions.

A senior project finance executive noted that “policy-driven cost uncertainty directly affects bankability.”

Impact on Project Structuring

Developers may need to:

- Rework financial models.

- Lock in long-term supply contracts.

- Adjust bid strategies in auctions.

Ground-Level Impact: EPCs, MSMEs, and Jobs

EPC Contractors

Engineering, Procurement, and Construction (EPC) firms may face:

- Higher procurement costs.

- Supply delays.

- Contract renegotiations.

MSME Ecosystem

Smaller suppliers could:

- Benefit from localisation push.

- Struggle with compliance costs.

Job Creation vs Disruption

While the policy is expected to create manufacturing jobs, short-term disruptions may affect project execution employment.

State-Level Competition: The Manufacturing Race

States are actively competing to attract solar manufacturing investments.

Emerging Hubs

- Gujarat: Integrated solar parks and manufacturing clusters.

- Tamil Nadu: Strong industrial base.

- Andhra Pradesh: Policy incentives and land availability.

This competition could accelerate capacity expansion but also create regional imbalances.

Auction Dynamics and Market Behaviour

Shift in Bidding Strategy

Developers are expected to:

- Bid more conservatively.

- Factor in supply risks.

- Avoid aggressive tariff commitments.

DISCOM Response

State utilities (DISCOMs) may:

- Delay procurement decisions.

- Push for renegotiation.

- Prefer lower-cost alternatives.

This could affect the overall pace of solar deployment.

Global Context: Strategic Autonomy Over Cost Efficiency

India’s approach aligns with global trends:

- The United States is subsidising domestic manufacturing.

- Europe is prioritising supply chain resilience.

- Trade tensions are reshaping global solar flows.

The era of ultra-cheap, globally sourced solar equipment is gradually shifting.

Three Possible Future Scenarios

1. Smooth Transition

- Rapid capacity expansion.

- Limited tariff increase.

- Stable project pipeline.

2. Disruptive Adjustment

- Supply shortages.

- Tariff spikes.

- Delayed projects.

3. Policy Recalibration

- Deadline extensions.

- Partial import relaxation.

- Hybrid sourcing models.

Related Links

Solar-to-Hydrogen ROI: Is it Finally Cheaper to Store Energy as Gas than in Batteries?

Electrolyzer Incentives: Decoding the ₹4,440 Crore Push for India’s Green Hydrogen Ecosystem

Key Risks to Watch

- Delays in manufacturing capacity expansion.

- Technology gaps in advanced cells.

- Global price volatility.

- Policy uncertainty.

FAQs

Will tariffs definitely rise by 50 paisa?

No. It is an estimate based on current cost structures and may change.

Why is ALMM expanding to cells?

To strengthen domestic manufacturing and reduce import dependence.

Will solar growth slow down?

Possibly in the short term, but long-term growth remains strong.

Who benefits the most?

Domestic manufacturers and integrated players.