India’s rapid expansion in solar manufacturing has raised a critical question: can the country become the world’s third-largest solar hub?

The Domestic Manufacturing Boom—fuelled by policy incentives, rising demand, and geopolitical shifts—is reshaping the renewable energy sector, though structural and technological challenges remain.

The Domestic Manufacturing Boom Gains Momentum

India’s solar manufacturing sector has expanded at an unprecedented pace over the past decade. From a limited base, the country has built substantial capacity in solar module production, supported by both public policy and private investment.

The Domestic Manufacturing Boom reflects a strategic shift towards self-reliance in clean energy technologies. Government officials have emphasised that reducing dependence on imports is essential for energy security and economic resilience.

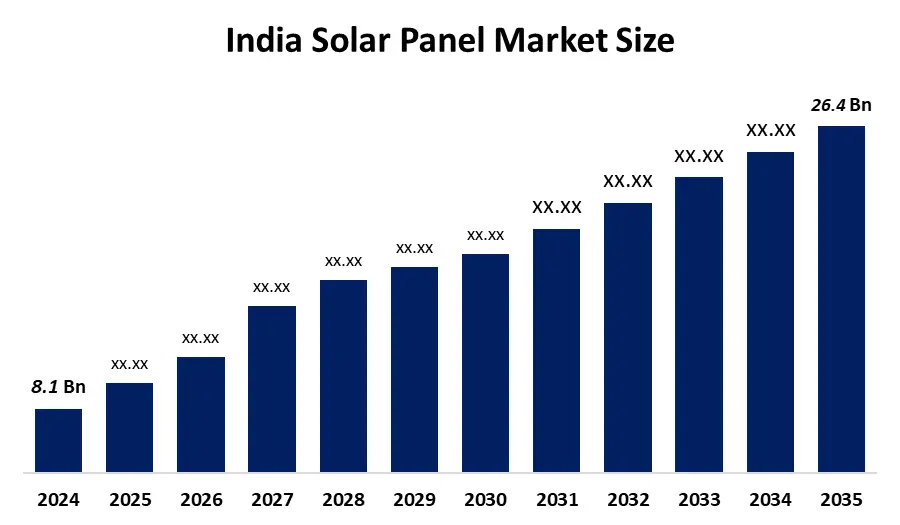

India’s solar ambitions are also tied to its climate commitments. The country aims to achieve 500 gigawatts of non-fossil fuel capacity by 2030, with solar energy expected to contribute the largest share.

Policy Framework: Incentives and Protection Measures

Production-Linked Incentive (PLI) Scheme

The Production-Linked Incentive (PLI) scheme has emerged as a cornerstone of India’s solar manufacturing push. It provides financial incentives to companies that establish or expand domestic manufacturing capacity, particularly across the solar value chain.

According to government statements, the scheme is designed not only to increase capacity but also to promote technological advancement and efficiency.

Tariffs and Import Controls

India has also implemented customs duties on imported solar equipment and enforced the Approved List of Models and Manufacturers (ALMM). These measures aim to protect domestic producers and encourage local sourcing.

Energy analysts note that such policies have significantly altered market dynamics, making domestic manufacturing more viable.

Demand Growth: A Strong Domestic Foundation

India’s solar installation rates have increased steadily, making it one of the fastest-growing renewable energy markets globally.

Large-scale solar parks, rooftop systems, and corporate renewable procurement are driving demand. State governments continue to announce new projects, while private companies are increasingly adopting solar energy to meet sustainability goals.

This strong domestic demand provides a reliable market for manufacturers, reducing exposure to global price volatility.

State-Level Manufacturing Clusters Emerging

India’s solar manufacturing expansion is not uniform. Several states are emerging as key hubs:

- Gujarat: Leading in large-scale manufacturing parks and port access.

- Tamil Nadu: Strong industrial ecosystem and skilled workforce.

- Andhra Pradesh: Land availability and policy support.

- Rajasthan: Proximity to large solar installations.

These clusters benefit from infrastructure, logistics, and policy incentives. Experts say regional specialisation could strengthen India’s manufacturing ecosystem.

Global Context: Competing with Established Leaders

The global solar manufacturing industry remains highly concentrated, with China dominating most segments of the supply chain. The United States and European Union have recently increased investments in domestic manufacturing, driven by concerns over supply chain resilience.

India’s position is improving, particularly in module manufacturing. However, experts caution that achieving global leadership requires deeper integration across the supply chain.

Supply Chain Gaps Remain a Key Constraint

Dependence on Imports

Despite the Domestic Manufacturing Boom, India continues to rely heavily on imports for upstream components such as wafers and polysilicon.

This dependence exposes the industry to external risks, including price fluctuations and geopolitical tensions.

Need for Integrated Manufacturing

Industry leaders have called for investments in upstream manufacturing to create a fully integrated supply chain. Such integration would improve cost competitiveness and reduce vulnerability to supply disruptions.

Technology Transition: Keeping Pace with Innovation

The solar industry is evolving rapidly, with new technologies such as TOPCon and heterojunction cells improving efficiency and performance.

Indian manufacturers face the challenge of adopting these technologies quickly. Failure to upgrade could reduce competitiveness in global markets. Experts emphasise that continuous investment in research and development is essential for long-term success.

Financing the Solar Manufacturing Push

Building a competitive solar manufacturing ecosystem requires significant capital investment. Industry estimates suggest billions of dollars are needed to develop integrated facilities.

Public sector banks, private investors, and international financial institutions are increasingly supporting renewable energy projects. However, access to affordable financing remains a concern for smaller firms.

A senior banking executive noted that “long-term policy clarity and stable returns are critical to attracting sustained investment in manufacturing.”

Employment and Economic Impact

The Domestic Manufacturing Boom is expected to generate substantial employment opportunities. Solar manufacturing, installation, and maintenance collectively create jobs across skill levels.

Government estimates suggest that the renewable energy sector could employ millions of people by the end of the decade.

In addition to direct employment, the sector also supports ancillary industries such as logistics, engineering, and raw material supply.

Environmental and Sustainability Considerations

While solar energy is central to India’s clean energy transition, manufacturing processes also have environmental impacts. Policymakers and industry stakeholders are increasingly focusing on sustainable manufacturing practices, including recycling of solar panels and responsible sourcing of materials.

Experts highlight the need for lifecycle assessments to ensure that solar manufacturing remains environmentally beneficial.

Geopolitical Factors and Supply Chain Diversification

Global geopolitical shifts are influencing the solar industry. Many countries are seeking alternatives to China-dominated supply chains, creating opportunities for India.

Trade partnerships and strategic alliances could enhance India’s position as a reliable supplier. However, competition from other emerging manufacturing hubs remains strong.

Risk of Overcapacity and Market Consolidation

Rapid expansion has raised concerns about potential overcapacity. Industry observers warn that manufacturing capacity may outpace demand in the short term.

This could lead to price pressures and consolidation within the industry. Smaller firms may face challenges in maintaining profitability. Similar trends have been observed in other global markets, where rapid growth has been followed by industry restructuring.

Related Links

PM Surya Ghar 2026 Update: How to Bypass DCR Certificates and Get Faster Subsidy Approvals

Solar Pumps: The KUSUM Advantage: How to Apply for Subsidized Solar Pumps in Your State

Expert Views: Optimism with Caution

Experts offer mixed assessments of India’s prospects. Some believe the country is well-positioned to become a major global hub, citing strong policy support and growing demand.

Others highlight structural challenges that must be addressed, including supply chain integration and technological advancement.An energy policy expert said, “India’s progress is significant, but becoming the third-largest solar manufacturing hub requires sustained investment and coordinated policy action.”

India’s solar sector has entered a phase of rapid expansion, driven by the Domestic Manufacturing Boom. The country has made notable progress in building manufacturing capacity and strengthening its position in the global renewable energy landscape.

However, achieving the status of the world’s third-largest solar hub will depend on addressing critical challenges, including supply chain gaps, technology adoption, and global competitiveness.

The outlook remains promising, but the path forward requires sustained effort, strategic investment, and policy consistency.