India’s rooftop solar expansion is entering a decisive phase, where financing strategy is as important as installation itself. The Surya Ghar vs. Private Loans comparison—Surya Ghar subsidy versus private loans—is increasingly shifting toward a hybrid model.

Experts say combining government subsidy with collateral-free solar loans is the most financially efficient approach for households in 2026.

Hybrid Solar Financing Is Redefining Household Energy Economics

The PM Surya Ghar: Muft Bijli Yojana provides upfront subsidies to reduce the cost of rooftop solar systems. At the same time, banks and NBFCs are offering collateral-free loans to finance remaining expenses.

Financial experts increasingly recommend combining these tools. This hybrid model reduces initial investment while maintaining liquidity and improving long-term financial outcomes.

Subsidy Structure Under Surya Ghar Scheme

The scheme provides structured financial support:

- ₹30,000 for 1 kW

- ₹60,000 for 2 kW

- Up to ₹78,000 for 3 kW+

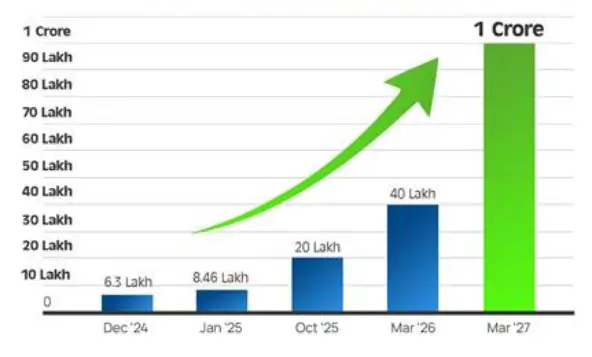

Subsidies can cover up to 40% of installation costs, depending on system size and configuration.The government aims to solarise one crore households, making rooftop solar a central component of India’s energy strategy.

Collateral-Free Solar Loans: Closing the Affordability Gap

Banks and NBFCs are offering specialised solar loans.

Typical Loan Features

- Loan size: ₹2–6 lakh.

- Interest rate: ~6.5%–9%.

- Tenure: Up to 10 years.

- No collateral for smaller loans.

These loans reduce the barrier of high upfront costs, enabling wider adoption.

Why the Hybrid Model Works Best

1. Lower Upfront Cost + Preserved Savings

Instead of paying ₹2 lakh upfront, households can:

- Use subsidy to reduce capital requirement.

- Use loans to spread remaining cost.

This preserves savings for emergencies or investments.

2. Cash Flow Neutrality

Electricity savings often match or exceed EMI payments.

Example:

- EMI: ₹3,000/month.

- Savings: ₹3,000–₹4,000/month.

This allows households to adopt solar without increasing monthly expenses.

3. Faster Payback Period

- Without subsidy: 6–8 years.

- With hybrid model: 3–5 years.

This significantly improves financial viability.

Sensitivity Analysis: What Happens If Assumptions Change?

Financial outcomes depend on multiple variables:

Key Factors

- Electricity tariff increases.

- Interest rate changes.

- Solar generation efficiency.

Scenario Insight

- Higher tariffs → faster ROI.

- Lower generation → longer payback.

- Higher interest → reduced net savings.

Experts recommend conservative assumptions when planning solar investments.

Panel Degradation and Long-Term Performance

Solar panels degrade over time.

Typical Degradation

- ~0.5% to 0.7% annually

Impact

- Slight reduction in output.

- Gradual decline in savings.

However, systems typically maintain 80–85% efficiency even after 20–25 years.

Hidden Costs Often Ignored

While solar is marketed as low-cost, some expenses are often overlooked:

- Inverter replacement after 8–10 years.

- Cleaning and maintenance.

- Net metering charges (in some states).

Including these costs provides a more realistic financial picture.

DISCOM and Net Metering Risks

Savings depend heavily on local electricity distribution companies (DISCOMs).

Key Issues

- Delays in net meter installation.

- Caps on export units.

- Policy variability across states.

These factors can influence actual financial returns.

Insurance and Risk Protection

Solar systems are long-term assets.

Insurance Options

- Covers damage from weather, fire, theft.

- Costs ~₹1,000–₹3,000 annually.

Experts recommend insurance to protect investment.

Urban vs Rural Adoption Dynamics

Urban Areas

- Higher electricity tariffs.

- Faster ROI.

- Greater awareness.

Rural Areas

- Lower tariffs.

- Slower payback.

- Infrastructure challenges.

Policy support may need to adapt for rural adoption.

Carbon Savings and Environmental Value

A typical 3 kW system:

- Reduces ~3–4 tonnes of CO₂ annually.

Over 20 years, this contributes significantly to emission reduction goals. Future markets may allow households to monetise carbon savings.

Vendor Ecosystem and Quality Control

Execution quality is critical.

Challenges

- Variability in installation standards.

- Limited after-sales support.

Best Practice

- Choose government-approved vendors.

- Verify certifications and warranties.

Financing Comparison: Cash vs Loan vs Hybrid

| Model | Upfront Cost | ROI Speed | Liquidity |

|---|---|---|---|

| Cash Purchase | High | Moderate | Low |

| Loan Only | Medium | Slow | Medium |

| Hybrid Model | Low | Fast | High |

Experts consistently favour the hybrid approach.

Macroeconomic Impact: Why This Matters

The hybrid financing model supports:

- Energy independence.

- Reduced subsidy burden over time.

- Job creation in solar sector.

- Growth of green finance ecosystem.

It aligns with India’s climate and economic goals.

Global Perspective

India’s approach is being closely watched globally. Few countries combine:

- Direct subsidy.

- Low-cost financing.

- Mass adoption strategy.

This could become a model for other developing economies.

Related Links

Mini Solar Light Trap: Buy Online for Pest Control in Farms Ends Pest Troubles Forever

Solar Waste Management: Are You Ready for India’s New Mandatory Panel Recycling Laws?

Risks and Limitations (Balanced View)

Key Risks

- Policy changes.

- Loan interest fluctuations.

- Vendor reliability issues.

Mitigation

- Careful planning.

- Financial modelling.

- Choosing trusted partners.

Context and Source Reference

The subsidy structure, financing models, cost analysis, and policy insights presented in this article are based on the detailed source material provided.

In 2026, the question is no longer whether to choose subsidy or loans—it is how to combine them effectively.

The hybrid model of Surya Ghar subsidy plus collateral-free solar loans offers the best balance of affordability, cash flow, and long-term returns. As rooftop solar adoption accelerates, this financing strategy is emerging as the cornerstone of India’s clean energy transition.