India’s renewable energy expansion has intensified investor interest in solar stocks, particularly Tata Power Company Ltd and Adani Green Energy Ltd.

As 2026 approaches, analysts are examining financial strength, debt levels, return ratios and growth pipelines to answer a pressing question: which solar giant offers a stronger investment case in a rapidly evolving clean energy market?

India’s Renewable Momentum Sets the Context

India aims to reach 500 gigawatts (GW) of non-fossil fuel capacity by 2030, according to official government targets. Solar power is expected to contribute the largest share of that expansion.

Data from the Ministry of New and Renewable Energy (MNRE) show that India’s installed solar capacity has grown substantially over the past decade. The International Energy Agency (IEA) has described India as one of the fastest-growing solar markets globally.

This macro backdrop frames the Tata Power or Adani Green comparison. However, Tata Power and Adani Green operate under distinct financial and strategic frameworks.

Tata Power or Adani Green: Business Model and Revenue Structure

The Tata Power or Adani Green debate begins with structure and revenue mix.

Tata Power Company Ltd

Tata Power Company Ltd, part of the Tata Group, operates across power generation, transmission, distribution, rooftop solar, electric vehicle charging and grid services.

The company generates revenue from regulated distribution businesses in Mumbai, Delhi and other regions. These segments provide relatively predictable income.

Renewable energy is an expanding but not exclusive component of Tata Power’s portfolio. The company has publicly stated its intention to significantly increase renewable capacity over the coming years.

Adani Green Energy Ltd

Adani Green Energy Ltd (AGEL) is a focused renewable energy developer. Its business model revolves almost entirely around solar and wind projects backed by long-term power purchase agreements (PPAs).

AGEL’s growth strategy emphasises rapid capacity addition and scale leadership. The company has outlined long-term targets approaching 45–50 GW of renewable capacity.

This pure-play model offers concentrated exposure to renewable growth, but also increases sensitivity to financing costs and execution risks.

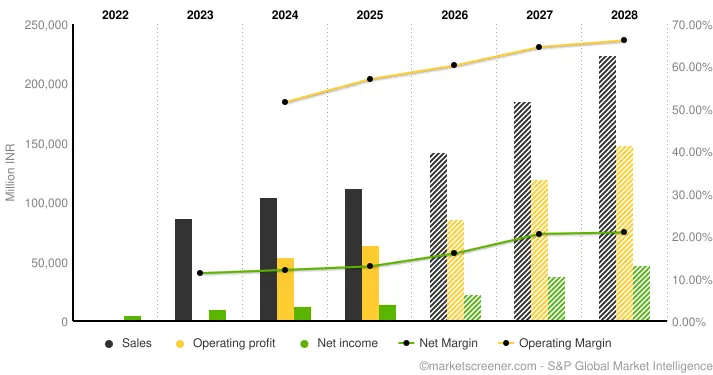

Financial Metrics: Revenue Growth and Profitability

Recent financial disclosures show that Tata Power’s consolidated revenue growth has remained steady, supported by diversified income streams.

Adani Green has demonstrated faster renewable capacity growth. However, quarterly earnings have occasionally fluctuated due to higher interest expenses associated with expansion.

Return on equity (ROE) metrics reflect structural differences. Tata Power’s diversified operations tend to generate moderate but stable returns. Adani Green’s returns can be influenced more heavily by leverage and project commissioning cycles.

Financial analysts emphasise evaluating operating cash flow rather than relying solely on net profit figures.

Debt, Cash Flow and Capital Allocation

Renewable infrastructure requires large upfront investment. Tata Power benefits from distribution earnings and regulated returns that help fund renewable expansion. Its capital expenditure programme is phased and integrated with existing operations.

Adani Green’s expansion strategy has relied on substantial borrowing and capital raising. This enables rapid growth but increases sensitivity to interest rate cycles.

Investors often examine debt-to-equity ratios, interest coverage and free cash flow generation when comparing the Tata Power or Adani Green options.

Dividend Policy and Shareholder Returns

Tata Power has historically maintained dividend payouts, reflecting its utility heritage and diversified earnings. Adani Green has focused primarily on reinvesting earnings into growth. Dividend payments have not been a central component of its shareholder strategy.

For income-focused investors, dividend continuity may influence preference.

Valuation Multiples and Market Expectations

Both companies trade at valuation levels reflecting renewable growth expectations. High price-to-earnings (P/E) multiples often signal anticipated future expansion. However, analysts caution that elevated valuations require sustained earnings growth to justify premiums.

Market participants frequently compare enterprise value to EBITDA ratios to assess capital efficiency across infrastructure firms. Volatility in share prices can widen valuation gaps, particularly during periods of macroeconomic uncertainty.

Governance, Transparency and Market Confidence

Corporate governance plays a role in investor perception. Tata Power benefits from the Tata Group’s longstanding corporate governance reputation and diversified board oversight.

Adani Group entities have faced international scrutiny in recent years, although the group has publicly denied wrongdoing in various instances. Such developments have occasionally influenced market sentiment. Governance assessments often affect institutional investment flows.

Scenario Analysis: What Could Shape 2026 Outcomes?

Scenario 1: Strong Policy Continuity and Low Interest Rates

If renewable incentives remain stable and borrowing costs ease, high-growth developers such as Adani Green could benefit disproportionately.

Scenario 2: Elevated Interest Rates and Market Volatility

In a higher-rate environment, leveraged expansion models may face margin pressure. Diversified companies such as Tata Power may demonstrate relative resilience.

Scenario 3: Distributed Solar Acceleration

If rooftop and decentralised generation expand rapidly, Tata Power’s integrated presence in distribution and rooftop solar may provide an advantage.

ESG and Sustainability Considerations

Environmental, Social and Governance (ESG) metrics increasingly influence capital allocation decisions.

Both companies contribute to renewable capacity growth and emissions reduction. However, ESG rating agencies evaluate broader governance frameworks, transparency and risk management. Global funds often incorporate ESG screening before allocating capital to infrastructure firms.

Risks Across Both Companies

- Policy changes affecting tariffs or subsidies.

- Delays in power purchase agreement payments.

- Project execution challenges.

- Commodity price fluctuations affecting input costs.

- Valuation corrections during market downturns.

A Mumbai-based renewable energy analyst noted, “India’s solar expansion is structural. The differentiation lies in financial discipline and capital efficiency.”

Long-Term Structural Drivers

India’s rising electricity demand, urbanisation and industrial expansion underpin renewable growth.

The government’s push for domestic solar manufacturing and grid modernisation strengthens sector fundamentals. Both Tata Power and Adani Green are central participants in this transition.

Related Links

Growth Ambition or Balanced Stability?

The Tata Power or Adani Green face-off between Tata Power and Adani Green ultimately reflects investor priorities. Adani Green offers concentrated renewable exposure and aggressive capacity expansion. This may appeal to investors with higher risk tolerance seeking strong growth.

Tata Power provides diversified revenue streams, dividend history and comparatively stable earnings, potentially appealing to investors prioritising risk-adjusted returns.

Both companies align with India’s long-term clean energy ambitions. The better buy for 2026 will depend less on headline capacity targets and more on financial execution, leverage management and policy continuity.