Vikram Solar Limited has signed a ₹2,000 crore agreement to procure 2 gigawatts (GW) of solar cells from Jupiter International, strengthening its domestic supply chain amid rising renewable demand.

The Vikram Solar Signs Massive Agreement deal comes as India accelerates its solar manufacturing push, prompting investors to assess whether this scale-up move can drive sustained earnings growth.

The ₹2,000 Crore Vikram Solar Signs Massive Agreement Agreement: What We Know

Vikram Solar announced a 2GW solar cell procurement agreement valued at approximately ₹2,000 crore with Jupiter International Limited, a domestic solar cell manufacturer. According to company disclosures filed under Securities and Exchange Board of India (SEBI) regulations, the transaction ensures supply of ALMM-compliant crystalline silicon cells, including TopCon and mono PERC technologies.

The agreement is structured as a supply arrangement rather than an equity partnership. The company clarified that Jupiter International is not a related party, addressing corporate governance considerations.

At 2GW, the order represents a significant volume relative to India’s domestic cell manufacturing capacity. Industry analysts estimate that 2GW can support module production worth several thousand crores in downstream revenue, depending on market pricing.

Why This Deal Matters in India’s Solar Ecosystem

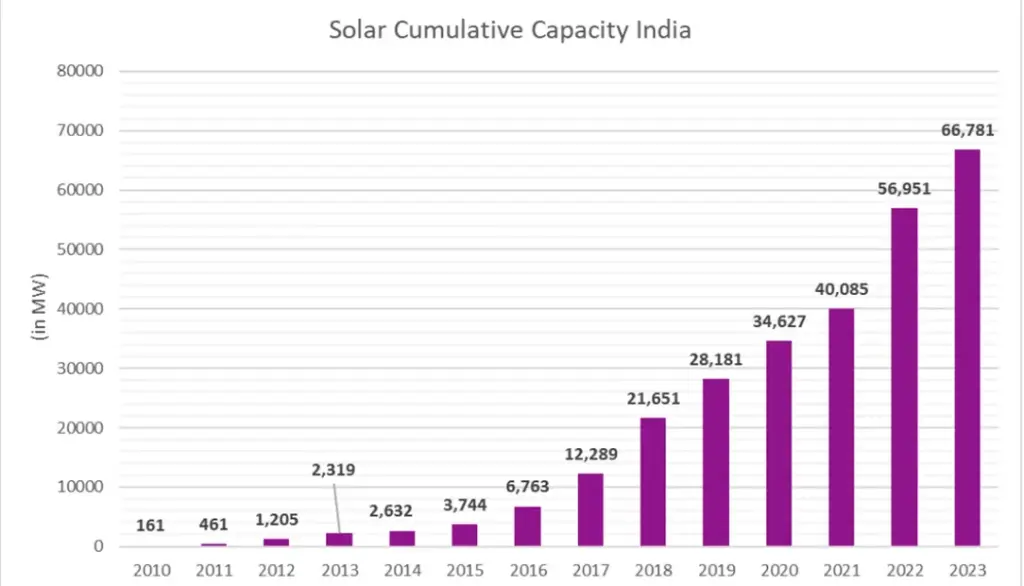

India’s renewable sector has witnessed rapid expansion. The government aims to achieve 500 GW of non-fossil fuel capacity by 2030, with solar expected to contribute a substantial portion.

However, a structural imbalance persists between module assembly and solar cell manufacturing. According to data from the Ministry of New and Renewable Energy (MNRE), module manufacturing capacity has grown faster than cell production under the Production Linked Incentive (PLI) scheme.

This gap has forced many manufacturers to rely on imported cells, exposing them to currency volatility, trade risks and supply chain disruptions. By securing 2GW of domestic cell supply, Vikram Solar reduces dependence on imports and aligns with policy priorities under the “Make in India” initiative.

Technology Strategy: TopCon and mono PERC

The agreement covers advanced TopCon cells and widely used mono PERC cells. TopCon technology offers higher efficiency and improved performance under low-light conditions. The International Energy Agency (IEA) has reported increasing global adoption of high-efficiency cell technologies as markets shift towards premium modules.

Mono PERC remains cost-competitive and is extensively used in utility-scale projects. By procuring both technologies, Vikram Solar maintains flexibility across project types, balancing cost and efficiency considerations.

Financial Impact: Revenue Visibility and Margin Considerations

Revenue Pipeline Strengthening

Assuming stable module prices, 2GW of cell-backed production capacity could generate significant incremental revenue. Solar module pricing fluctuates, but industry estimates suggest that multi-gigawatt output can translate into revenue in the range of ₹5,000–₹7,000 crore over the execution period.

The agreement therefore enhances revenue visibility, especially in a tender-driven market where assured supply is critical for bidding competitiveness.

Margin Dynamics

However, procurement pricing terms will determine profitability. Solar manufacturing margins are influenced by:

- Polysilicon and wafer prices

- Global supply-demand cycles

- Currency fluctuations

- Domestic pricing competition

If cell procurement costs rise while module selling prices decline, margins could narrow. Investors typically monitor gross margin trends in quarterly earnings to assess pricing discipline.

Capital Expenditure and Integration Plans

Beyond procurement, Vikram Solar has previously indicated expansion plans for integrated manufacturing capacity. Industry disclosures suggest potential investments in backward integration into cell production in the coming years.

Backward integration could:

- Improve margin control

- Reduce supplier dependency

- Enhance competitiveness in export markets

However, such integration requires substantial capital expenditure. Investors must assess funding sources, debt levels and execution timelines.

Order Book, EPC Exposure and Diversification

Vikram Solar operates not only as a module manufacturer but also as an engineering, procurement and construction (EPC) contractor. This vertical integration allows participation across the project lifecycle.

Order book growth will be a key indicator. A strong order pipeline ensures that secured cell supply translates into revenue realisation. Diversification across utility-scale projects, rooftop installations and export markets can also cushion cyclical fluctuations in any single segment.

Is This a Multibagger in the Making?

The term “multibagger” implies substantial long-term capital appreciation. Such outcomes depend on consistent earnings growth, scalable operations and favourable valuation multiples.

Factors Supporting Potential Upside

- Strong Domestic Demand: India’s renewable targets underpin long-term solar deployment.

- Policy Tailwinds: PLI incentives and ALMM requirements encourage domestic sourcing.

- Supply Assurance: The 2GW deal addresses near-term production risk.

Key Risks

- Execution Risk: Delays in expansion or quality issues could impact reputation.

- Competitive Landscape: Multiple Indian players are expanding capacity simultaneously.

- Global Price Volatility: Module prices remain sensitive to international supply shifts.

Equity strategists caution that renewable manufacturing stocks often experience sharp valuation swings tied to policy cycles and global commodity trends.

Peer Comparison and Sector Competition

India’s solar manufacturing space includes companies such as Adani Solar, Waaree Energies and Tata Power Solar. Many are expanding module and cell capacities under government incentives.

Competitive intensity may affect pricing power. Companies with integrated supply chains and technology upgrades could enjoy relative advantages. Analysts observe that scale alone does not guarantee profitability; cost management and operational efficiency remain decisive.

Export Opportunities and Trade Risks

Indian manufacturers have targeted export markets amid global efforts to diversify supply chains beyond China. However, trade policies in the United States and Europe can introduce uncertainty.

Recent global tariff actions against certain solar imports illustrate the geopolitical sensitivity of renewable supply chains. While Vikram Solar’s current agreement focuses on domestic sourcing, export strategy remains a key factor in long-term valuation.

Sustainability and ESG Considerations

Institutional investors increasingly evaluate environmental, social and governance (ESG) metrics.

Domestic sourcing of ALMM-compliant cells aligns with India’s industrial policy and reduces supply chain risk. Transparent governance disclosures regarding related-party transactions and procurement terms also support investor confidence.

What Analysts Will Watch Next

Investors and analysts are likely to monitor:

- Quarterly financial results and margin trends

- Capacity utilisation rates

- Debt and working capital levels

- Execution of expansion projects

- Changes in global module pricing

Clear management communication regarding procurement pricing and order conversion will be critical.

Broader Implications for India’s Renewable Manufacturing

The 2GW procurement underscores the transition from import dependence toward domestic value chain strengthening. It signals confidence in India’s solar manufacturing base.

Such agreements also reflect industry maturity, where long-term supply arrangements replace spot-market volatility. For policymakers, large domestic procurement deals indicate traction in manufacturing incentives.

Related Links

Hidden Gems: Top 5 Smallcap Renewable stocks that could turn into the next multibagger opportunities

Vikram Solar’s ₹2,000 crore 2GW solar cell agreement strengthens supply stability and aligns with India’s renewable expansion strategy. The Vikram Solar Signs Massive Agreement deal enhances near-term production visibility but does not automatically ensure multibagger returns.

Long-term shareholder value will depend on disciplined execution, margin stability, technological competitiveness and prudent capital management.

Investors should evaluate fundamentals and risk factors carefully rather than relying solely on headline scale.