India’s solar industry sharply increased imports of photovoltaic modules in the months preceding the April 2024 enforcement of the Approved List of Models and Manufacturers (ALMM) policy, according to data from the Ministry of New and Renewable Energy (MNRE).

Developers rushed to procure lower-cost imported panels before stricter domestic sourcing rules took effect, highlighting the ongoing tension between India’s renewable-energy expansion and its ambition to build a domestic solar manufacturing industry.

India’s Solar Module Imports

| Key Fact | Detail |

|---|---|

| ALMM enforcement | Reinstated April 1 2024 |

| Import surge | Developers accelerated purchases before the deadline |

| Total solar imports | Over $10 billion in recent fiscal years |

| Solar capacity | Over 100 GW installed capacity in India |

| Main supplier | China remains dominant in module supply |

India’s Solar Module Imports Surged Ahead of the 2024 ALMM Deadline

Solar module imports rose sharply in the fiscal year preceding the ALMM enforcement deadline, reflecting developers’ attempts to secure foreign equipment before the new rules applied.

Under the ALMM policy, solar projects supported by government programmes must use modules manufactured by companies included on a registry maintained by the Ministry of New and Renewable Energy.

Industry analysts say the policy is designed to promote domestic manufacturing while improving quality standards in India’s rapidly growing solar sector.

However, the regulation also created a temporary procurement window that developers used to import cheaper modules before the rules took effect.

“Whenever a major regulatory change approaches, project developers typically accelerate procurement,” said Raj Prabhu, chief executive of renewable-energy consultancy Mercom Capital Group, in commentary published by industry analysts.

Understanding the ALMM Policy

Purpose of the Regulation

The Approved List of Models and Manufacturers (ALMM) was introduced to strengthen domestic manufacturing capabilities and ensure that solar projects use high-quality equipment.

The policy restricts government-supported projects from using modules that are not listed in the ALMM registry. By requiring approved manufacturers, policymakers aim to create a stable market for domestic producers.

Officials say the measure also improves quality assurance by ensuring modules meet certain performance standards.

Suspension and Reinstatement

The ALMM requirement was temporarily suspended in 2023 after industry groups warned that domestic production capacity might not be sufficient to support India’s rapidly expanding solar deployment.

The government reinstated the rule from April 2024, arguing that new manufacturing capacity had been added and could now support domestic demand. This policy transition triggered a surge in imports before the rule returned.

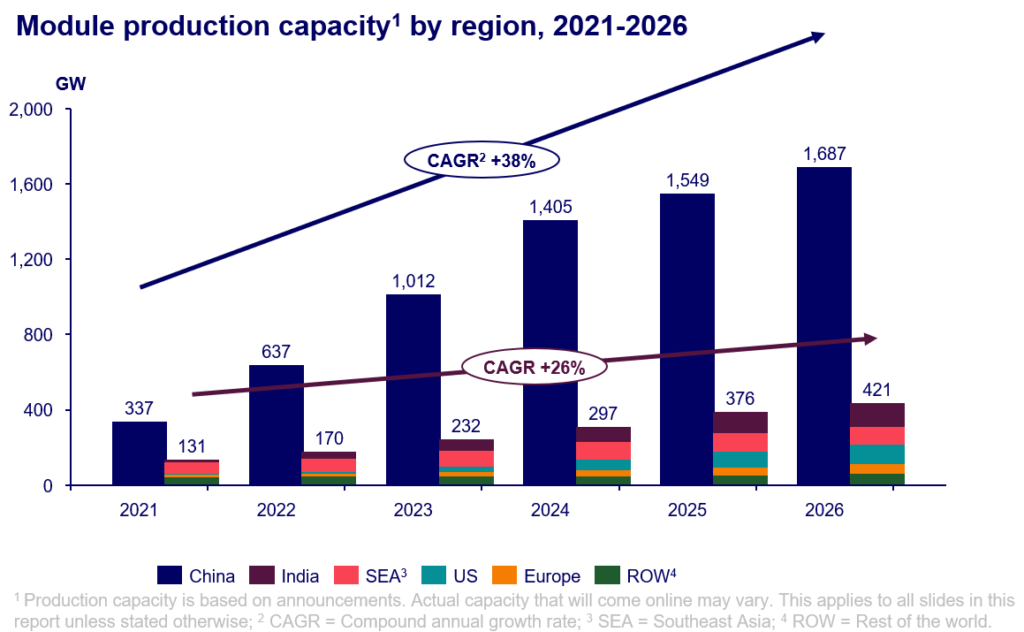

China’s Dominance in Global Solar Manufacturing

India’s reliance on imported solar modules reflects broader global supply chain dynamics. China dominates solar manufacturing worldwide, producing a majority of the world’s solar wafers, cells, and modules.

This dominance allows Chinese manufacturers to benefit from economies of scale and integrated supply chains. Industry analysts note that Chinese solar modules are often significantly cheaper than domestically manufactured alternatives.

Lower costs have made imported panels attractive for developers seeking to keep electricity tariffs competitive.

India’s Expanding Solar Energy Market

India’s solar sector has grown rapidly during the past decade. Solar energy has become one of the country’s fastest-growing electricity sources, driven by declining technology costs and government policy support.

Installed solar capacity has crossed 100 gigawatts, according to official statistics. Solar electricity generation also increased significantly during the past year, highlighting the sector’s rapid expansion.

Government planners see solar power as central to India’s strategy for reducing dependence on fossil fuels and meeting climate commitments.

Domestic Manufacturing Expansion

To support these ambitions, India has significantly expanded domestic solar manufacturing capacity. Industry reports indicate that the country added more than 10 gigawatts of new module manufacturing capacity during 2024, bringing total capacity close to 80 gigawatts.

However, solar cell manufacturing capacity remains far lower. This imbalance creates a supply-chain gap that forces module manufacturers to rely on imported cells. Experts say this structural challenge explains why imports remain high despite domestic production growth.

Production Linked Incentive (PLI) Scheme

The Indian government has also launched the Production Linked Incentive (PLI) scheme to boost domestic solar manufacturing. The programme provides financial incentives to companies investing in large-scale solar manufacturing facilities.

The policy aims to create vertically integrated production lines that manufacture wafers, cells, and modules within India. Energy analysts say the PLI scheme could help reduce import dependence in the long term. However, new factories may take several years to reach full production capacity.

Impact on Solar Project Economics

The surge in imports ahead of the ALMM deadline has implications for solar project economics. Lower-cost imported modules allow developers to bid aggressively in competitive electricity auctions.

These lower bids can reduce electricity tariffs for utilities and consumers. However, policymakers argue that domestic manufacturing capacity is essential for long-term supply security. Balancing cost competitiveness with domestic industrial development remains a key challenge.

Regional Solar Manufacturing Clusters in India

India’s solar manufacturing industry is concentrated in several key regions. Major production clusters have emerged in states such as:

- Gujarat

- Rajasthan

- Tamil Nadu

- Telangana

- Andhra Pradesh

These states host several large module assembly plants as well as new manufacturing facilities supported by government incentives. Industry observers say these clusters could help create an integrated solar manufacturing ecosystem in India.

Energy Security and Supply Chain Risks

Solar supply chains have become an increasingly important geopolitical issue. Countries around the world are seeking to diversify manufacturing away from concentrated supply hubs. India’s solar manufacturing strategy reflects these concerns.

By building domestic production capacity, policymakers hope to reduce vulnerability to international supply disruptions. However, analysts say global supply chains will likely remain interconnected for the foreseeable future.

Industry Perspectives

Renewable-energy developers and manufacturers hold differing views on the ALMM policy. Domestic manufacturers generally support the regulation, arguing that it protects local industry and encourages investment.

Developers, however, sometimes express concern that restrictions on imports could increase project costs. Energy analysts say a balance will be required to ensure both affordable electricity and strong domestic manufacturing.

Related Links

Beyond the Roof: Top 5 US urban solar trends transforming city living in 2026

Battery Storage Incentives: Get extra cash for pairing your solar with home batteries

Future Outlook for India’s Solar Industry

India has set ambitious renewable-energy targets for the coming decade.

Solar power will play a central role in meeting those goals.

Government planners aim to significantly expand solar capacity while also building a domestic manufacturing ecosystem.

Industry analysts say policies such as ALMM and the PLI scheme will shape the structure of India’s solar supply chain in the years ahead.

The surge in solar module imports ahead of the 2024 ALMM deadline illustrates the complex relationship between industrial policy and renewable-energy expansion. Developers rushed to secure affordable imported panels before stricter sourcing rules took effect, while policymakers pursued long-term goals of strengthening domestic manufacturing.

As India continues expanding its solar capacity, balancing affordability, supply security, and domestic industrial growth will remain a central challenge for the country’s energy transition.